Sweden’s defence industrial model is highly capable but structurally constrained. Dr. Rebecca Harding examines why 380 firms, an export-orientation, and sovereign capability sit alongside acute SME access-to-finance risk.

Dr. Rebecca Harding | April 2026

Executive Summary

Sweden’s defence industrial model is highly capable but structurally constrained. A fully privatised, export-oriented sector with around 380 firms (including 80 advanced exporters) retains sovereign capability across key platforms but faces growing difficulty scaling to meet NATO and geopolitical demands.

The core issue is not a lack of capital, but its misallocation. Despite rising defence spending (targeting 3.5% of GDP by 2030), funding is concentrated on procurement rather than enterprise financing, leaving persistent gaps in working capital, early-stage growth finance, and scalable debt for SMEs.

SMEs are critical but under-financed. Around 200 SMEs are now active in defence exports, yet many—particularly in lower-tier supply chains—struggle to access bank lending, with up to 50% not seeking debt finance at all.

Current financing structures are poorly aligned with sector needs. Venture capital is over-supplied relative to viable scalable opportunities, while debt-based, export, and supply chain finance remain insufficient—creating risks of valuation distortions and underinvestment in production capacity.

European funding mechanisms are not well suited to Sweden’s model. Grant-based, collaboration-driven instruments (e.g. EDF) risk distorting incentives and lack the scale and flexibility required for a predominantly private-sector ecosystem.

Policy frameworks remain rooted in a peacetime economic model. Regulatory, procurement, and financing systems are not sufficiently adapted to the speed and scale required in the current security environment.

A shift toward market-compatible financing solutions is required. Priority should be given to guarantee-based lending, export finance, and supply chain finance that leverage commercial bank balance sheets and preserve private ownership structures.

Implications for DSRB: Sweden represents a strong use case for a non-intrusive, de-risking model, where the role of a multilateral institution is to unlock private capital—rather than deploy direct co-investment—thereby enabling SMEs to scale without equity dilution and strengthening NATO-aligned industrial capacity.

Introduction

Sweden’s defence industrial base is distinctive in its fully privatised structure, strong export orientation, and deep integration into dual-use innovation ecosystems. While this model has delivered high levels of technological capability and global competitiveness, it is increasingly challenged to scale to meet the demands of a rapidly evolving security environment, particularly following NATO accession and the intensification of geopolitical risk in Europe.

The sector comprises approximately 380 companies, including around 80 advanced technology exporters, with SMEs playing a growing but still under-recognised role in delivering innovation and supply chain resilience. Sweden retains full sovereign capability across key defence platforms, indicating that the industrial base has the capacity to scale—provided that appropriate financing mechanisms are in place.

Despite a significant increase in defence spending—targeting 3.5% of GDP by 2030—public funding is predominantly directed toward procurement rather than enterprise financing. As a result, critical gaps persist in working capital, early-stage growth finance, and scalable debt solutions, particularly for SMEs operating in lower tiers of defence supply chains. Existing regulatory and procurement frameworks remain rooted in a peacetime economic model, constraining the speed and flexibility required for industrial expansion.

At the same time, Sweden’s defence sector is highly export-driven, with military exports reaching SEK 28bn in 2025 and growing rapidly, supported by SME participation. However, current financing structures—particularly the dominance of venture capital—are poorly suited to this model. Evidence suggests an emerging imbalance, with excess VC capital chasing limited scalable opportunities, while the more pressing need for debt-based, supply chain, and export finance remains unmet.

European funding instruments, such as the European Defence Fund (EDF), are also imperfectly aligned with Sweden’s market structure. Their grant-based, collaboration-driven approach risks distorting incentives and fails to provide the scale or flexibility required for a predominantly private-sector ecosystem.

The central policy implication is that Sweden’s defence financing gap is not one of capital scarcity, but of capital misallocation. Addressing this requires a shift toward market-compatible financial mechanisms, particularly guarantee-based lending, export finance, and supply chain funding solutions that leverage the strength of commercial banks and preserve private ownership structures.

Sweden represents a compelling use case for a non-intrusive, private-sector-aligned model of multilateral finance. Swedish banks are used to this type of multilateral framework through work in defence with the Nordic Investment Bank. Additional, as the private sector drives the industry itself, the means of increasing financing must enable rather than interfere with market operations. Rather than direct co-investment, the priority should be to de-risk lending and unlock balance sheet capacity within the banking system, enabling SMEs to scale without equity dilution. This approach would better reflect Sweden’s institutional preferences while addressing systemic financing gaps critical to national and allied security outcomes.

Sweden’s defence sector

Sweden’s defence sector is independent of the government and operates entirely in the private sector. Sweden does not have a security of supply strategy or a defence supply strategy. The government does not own or control companies within the defence sector, either in terms of its access to the sectors intellectual property development or in terms of in terms of placing an obligation for the sector to prioritise the requirements of the Swedish Armed Forces. It is therefore a fully privatised industry and while it does have national security obligations to prioritise procurement of aircraft, under-water vessels, strategic equipment and ammunition supply, it operates independently from government to deliver contracts globally.[1]

Recent data on the SME sector is hard to find in the public domain. However, it seems that there are around 380 companies in the Swedish defence ecosystem. 80 of these are exporters of advanced munitions, vessels, software, combat vehicles and surveillance systems.[2]

Emerging technologies, such as UAVs and space are dynamic and heavily concentrated in regional clusters making collaboration in R&D easier. Many of the 48 priority sectors that are core to Swedish competitiveness and resilience are in dual use areas such as semi-conductors, propulsion technologies, AI and medical technologies.[3]

According to SME-D the role of SMEs has not historically been as well understood in Sweden as it now needs to be in order to address the need to scale quickly and innovatively to meet the challenges that the country faces. The regulatory, financial and procurement systems reflect a peacetime economy and is poorly adapted to the current rapidly changing and threatening geopolitical backdrop in Europe.[4]

Sweden’s businesses are well-placed to take advantage of the opportunities associated with entry to NATO but need to be aware of the procurement and funding challenges associated with it according to Business Sweden.[5]

Sweden produces 100% of its sovereign capability in combat aircraft, infantry armoured vehicles, other armoured vehicles, self-propelled artillery, small surface combatants and attack submarines.[6] This suggests that with the right financing, supply chains and scalability do exist to scale.

Sweden’s defence spending and policy

The Swedish government has borrowed SEK 300bn to achieve the NATO target 3.5% of GDP spend on defence by 2030.[7] It is building stockpiles and rearming, specialising in swarm drones, modernising its transport and logistics system to enable full integration with NATO and encouraging innovation in advanced technologies such as AI and quantum to strengthen the nation’s cyber-security. It is also supporting collaboration between Bae systems and Bofors to develop self-propelled Howitzers.[8]

The Defence Industry Strategy is focused on building on the innovation strengths of the country by enhancing the collaborative potential between large and small businesses in the system, and building cooperation between industry and government to incentivise public and private investments around the country’s broader National Security Strategy. The defence budget has doubled since 2022, an increase which is largely around support for procurement rather than financial support to businesses. There is an acknowledgement that if the industry is to scale, there needs to be enhancements to the clusters and collaborative structures intrinsic to its ecosystem. This will mean an amended financial framework and better access to procurement for SMEs. In particular this could mean state investment as a means to creating security of supply alongside European frameworks and financial instruments.[9]

Sweden’s 2026 budget bill committed a further SEK 26.6bn (an 18% increase on 2025) in government military spending including a defence innovation fund.[10]

European instruments such as the EDF are not necessarily that well suited to Sweden’s specific funding needs according the FOI. The awards based model supports collaboration and networking in the EU and Norway, but not across Sweden’s whole defence and innovation network and creates market distortions by incentivising public sector priorities and creating winners and losers on a non-market basis.[11]

Sweden’s exports

Sweden’s defence sector is uniquely export oriented because Sweden itself has been historically a relatively small market until Russia invaded Ukraine, and because its businesses are independent of the government.

Sweden’s exports of military equipment stood at SEK 28bn in 2025; this number is expected to grow further in 2026.[12] According to EKN, export volumes have been increasing rapidly, especially amongst SMEs, with around 200 now involved in exporting activity associated with defence supply chains.

Swedish SMEs are highly innovative and able to take advantage of the growing defence markets across the world, and especially in NATO since it became a member. Between 2023 and 2024 alone, the industry grew by 55%.[13]

Finance

As the Swedish defence sector is in the private sector, non-public sector finance is critical to its development. Most of government spending goes into procurement rather than into working capital or defence and innovation solutions funding.

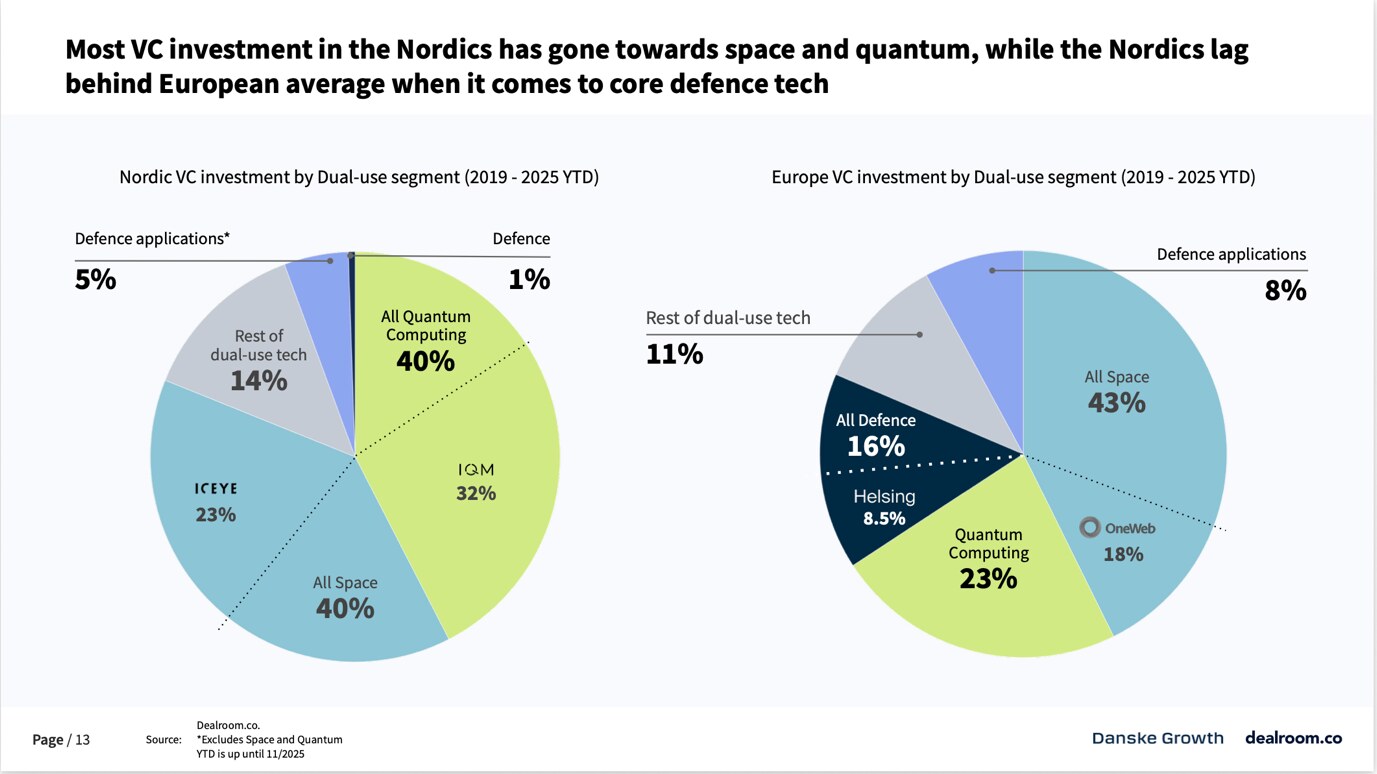

Large sums of money are going into the innovation base in Nordic nations because of the size of the market which in all dual use good is worth some $5.4bn across the region in 2025. There was some $563m invested in 2025 in dual use and defence. Nevertheless, Nordic nations generally lag behind the EU average in defence venture capital (Figure 1) and the amount invested in defence fell in 2025.[14]

Banks across Europe acknowledge their increased role in defence and security lending given the imperatives of the challenge but point to structural difficulties in funding defence which need to be overcome. These are not felt to be sustainability or ESG regulations as such although risk appetites amongst bank shareholders vary and the definitions of “controversial weapons” in regulatory frameworks needs to be clarified to “prohibited weapons.”[15]

SMEs operating across Europe report difficulties in accessing finance compared to other sectors and around 50% of those surveyed by the EU in a report published in 2024 said that they did not approach banks for debt-based financing.[16]

The Nordic Investment Bank (NIB) has altered its sustainability exclusions in its sustainability policy to include lending for conventional weapons and ammunition. This is in response to a recognition that the banking sector needs to do more and accordingly, it has provided Saab with a SEK 1.2bn loan to invest in R&D and capability development.[17] NIB has also provided investment into Lithuania’s defence systems and NIB acts as a coordinating mechanism between Baltic banks to improve access to debt and equity finance.[18]

SEB, Sweden’s largest bank, has also shifted its policies to allow funding of conventional and nuclear weapons if their development is based in a Nato country.[19] This includes an equity fund as well as debt-based finance.[20]

Swedish banks have increased their lending through multilateral lending and investment structures such as the NIB[21] to enable cross-border synergies within the region. The Swedish Defence Research Agency points out however, that more financial scale is needed to take advantages of opportunities across Europe and NATO[22] and that this funding should go beyond the constraints of location such as exist through the EDF.

Figure 1 — Source: Dealroom and Danske Growth, Nordic Defence Sector Tech Report 2025

Figure 1 — Most VC investment in the Nordics has gone towards space and quantum, while the Nordics lag behind European average when it comes to core defence tech. Source: Dealroom.co and Danske Growth, Nordic Defence Sector Tech Report 2025.

Defence start-ups in Sweden face a number of barriers including issues with procurement and regulation and certification, limited access to collaborative networks unless they are tied to a defence Prime, rapid increases in demand and a lack of early stage financing. While the government has stated in its strategy that the innovative strengths of the nation must be transformed into industrial power, the speed that these needs to be done means that extraordinary measures will be necessary. At present just SEK 1.3bn is spent on addressing some of these challenges from the total Swedish defence budgets and there is some commercial resistance to increased government investment in the whole process.[23]

Many start-ups argue they are bootstrapping and that current funding is inadequate.[24]

Some private equity investors have argued that there is too much VC funding out there and insufficient deal quality/venture scalability within the innovation base.[25] As a result, the vast expansion of the VC market is likely to end up with “too much money chasing too few deals” and push up the valuations. This has the potential to create a bubble unless the essential gap in working capital and debt-based finance is closed effectively and soon.

In other words, the means that the approaches to defence financing need to reflect the reality of the private sector base of Sweden’s industry itself. This may mean more by way of debt-based finance (supply chain and exports) and less in the form of VC. In particular, the export-oriented nature of the defence industry in Sweden suggests that whole sector now needs a different approach to guarantees and tailored financial solutions to make sure that the full scope of this exporting potential is realised according to EKN.[26] A new appetite amongst investors and banks means that there is strong impetus behind providing these flexible mechanisms to support provision of capital through supply chain and asset-based financing solutions.[27]

Conclusions for DSRB

Because the Swedish model does not encourage state intervention into markets, the defence industry is likely to benefit more from private sector led initiatives that provide guarantees rather than co-investment.

Sweden’s banks work within multilateral frameworks to fund defence such as the Nordic Investment Bank. Scaling the multilateral funding model provides access to a greater geographical spread of opportunities for funding that would be enhanced by scaled multilateral financial instruments.

There are gaps in many of the policy documents reviewed here around the access to finance for SMEs generally in Sweden, and for access to supply chain finance in particular. Yet policy does prioritise greater collaboration across and within supply networks in the country and beyond.

There is a tendency to consider innovation and VC as the beginning and end of all private sector defence solutions. However, Swedish businesses are highly export-oriented and participate in global supply chains. This means that the SMEs in lower tiers of supply chains are able to access working capital through guaranteed lending from commercial banks, rather than by ceding equity/diluting.

There are faults with a lot of the collaborative defence funding frameworks (like EDF) because they militate against the way in which the Swedish free market works to optimise international research and network capability. They over-encourage collaboration through grants but do not provide scale.

There is a lack of venture-scale businesses in defence and security everywhere but in Sweden in particular. Many of the smaller companies needing funding are not scalable in the sense used in VC or PE. This means that there is a known gap in funding for all the companies that provide specific parts of defence solutions in Sweden but are not fundable through VC in any long-term sense.

Artillery ammunition prices have risen several hundred percent since 2021. Dr. Rebecca Harding on how defence inflation is eroding NATO military capability.

Defence spending alone has modest and short-lived effects on growth. Dr. Rebecca Harding on why the STRUCTURE of defence finance is what turns spending into sustained resilience.

Sweden’s defence industrial model is highly capable but structurally constrained. Dr. Rebecca Harding examines why 380 firms sit alongside acute SME access-to-finance risk.

Germany’s defence SMEs face a systemic access-to-finance challenge that has become a strategic vulnerability. Dr. Rebecca Harding on the evidence and the mechanisms.