Germany’s defence SMEs face a systemic access-to-finance challenge that has become a strategic vulnerability. Dr. Rebecca Harding on the evidence, the mechanisms, and what multilateral instruments could unlock.

Dr. Rebecca Harding | 17 March 2026 | Chief Economic Advisor r.harding@dsrb.org

Executive summary

This document is based on a review of documentary evidence largely published since April 2025 on the Defence SME funding gap in Germany. The core findings are:

Defence production depends heavily on SMEs. In Germany, SMEs generate around 80% of defence industry turnover (about €23bn) and form the backbone of the defence supply chain.

These companies must finance production themselves before revenue arrives. SMEs often need to fund materials, inventory, certification, and production expansion months before payment, creating large upfront financing needs.

Bank lending to SMEs is tightening, not improving. 37.8% of German SMEs report restrictions on bank credit, the highest level since 2017, and only one in five SMEs even attempts to seek bank financing.

Defence order books are expanding faster than SME balance sheets. European defence company backlogs have grown from €103bn in 2017 to €291bn in 2024, implying about €50bn of backlog linked to German SMEs that must finance production capacity.

There is already a measurable financing gap. Estimates suggest €2–4bn in equity financing and €1–2bn in debt financing is missing for German defence SMEs, and this gap is likely to grow as the sector expands.

Defence spending is rising rapidly across Europe. However, the SME supply chains that manufacture much of the equipment lack sufficient access to credit to scale production. The clear risk here is that defence budgets can increase faster than industrial production capacity. The issue is therefore not a lack of demand for defence production, but a shortage of capital available to the companies that must expand manufacturing capacity.

Introduction

This document is a summary of documentary research scanning publications from banks, industry representative organisations and academia/think tanks to assess the scale of the defence SME funding gap in Germany. The German government voted for big changes in the way that defence would be funded in the country in March 2025. The publications that are assessed in this document are largely from after that date in order to give a realistic picture of the need for increased SME financing now in spite of the scale up of overall funding to defence that has taken place since the current administration came to power.

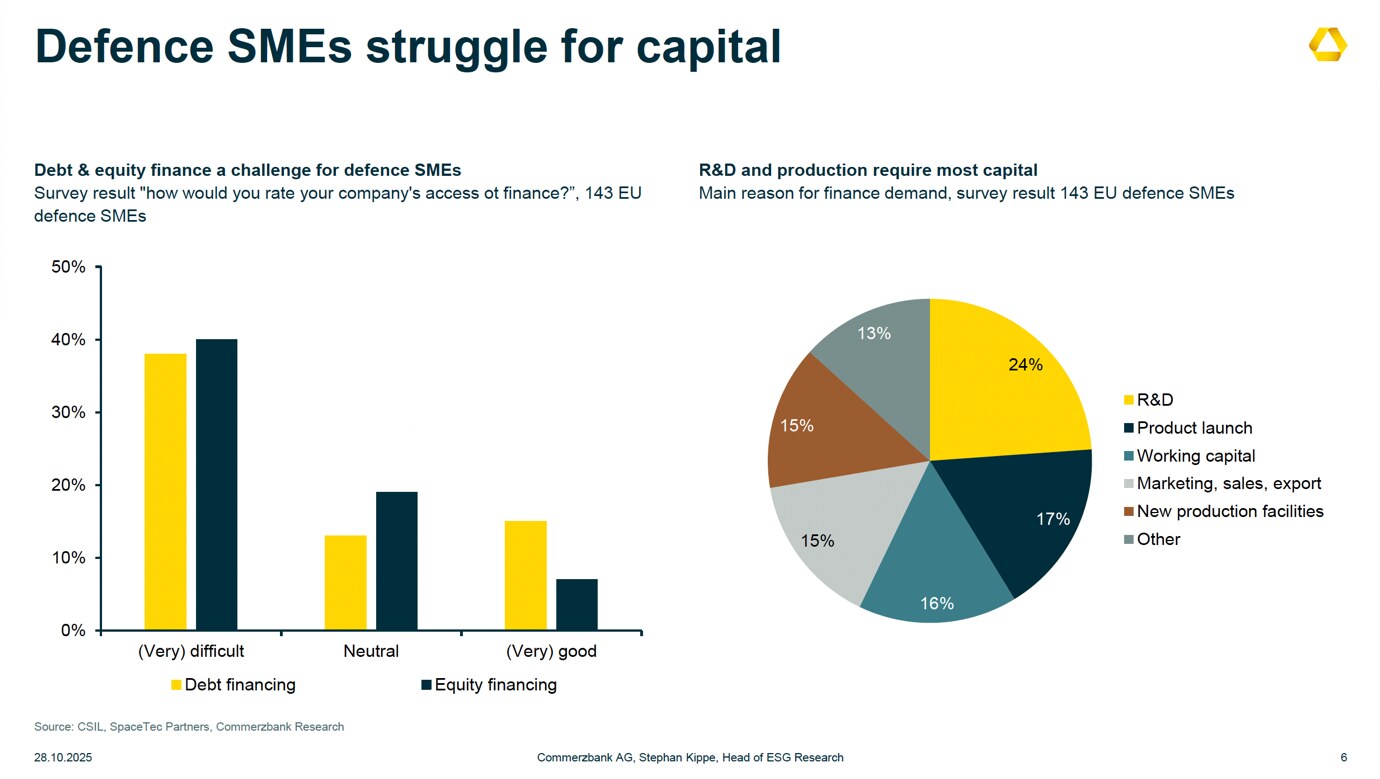

As highlighted by the Commerzbank, defence SMEs do not have the levels of capital across Europe generally that they need.

Commerzbank Research (Oct 2025) — Defence SMEs' challenges accessing debt & equity finance; R&D and production dominate demand for capital. Source: CSIL, SpaceTec Partners, Commerzbank Research.

Source – Commerzbank October 2025

For example, Commerzbank is one of Germany’s largest banks for funding SMEs through lending but cannot meet increased demand not for lack of willingness to fund, but because defence SMEs lack the capital depth and balance sheet strength to scale production in line with demand, particularly given long procurement cycles and high upfront investment needs. For banks, this creates a risk-return mismatch—lending to SME suppliers without direct access to government contracts is capital-intensive and difficult under current regulatory and cooperative financial frameworks, limiting the flow of credit precisely where it is most needed in the defence supply chain (https://www.commerzbank.de/konzern/was-uns-bewegt/unternehmerischer-erfolg/boombranche-ruestung.html).

German SMEs constitute around 80% of the current defence turnover in Germany which totals €23bn) and are currently facing a number of strategic and financing challenges according to LBBW:

Current order backlog at European defence companies rose to EUR 291bn in 2024. Assuming a stable share for Germany / DACH, this suggests a current backlog of around EUR 50bn for German SMEs. With around EUR 200bn per year of needed investments in Europe, one could expect this to increase the backlog for German SMEs by another EUR 40-50bn over the next ten years given they are primarily bank-financed and limited by their balance sheet size (as opposed to funding themselves in the market)

There are currently 400 members of the German defence association. This is expected to scale as innovative defence companies gain traction and manufacturing businesses transition to defence to around 2,000 businesses. This will at least double if not triple the anticipated financing requirements.

There are a number of critical points that are specific to Germany’s Defence Industrial Base:

First, the German defence sector is SME driven but dominated by systems integrators/Primes (https://research.handelsblatt.com/wp-content/uploads/2026/01/Sicherheit_u_Verteidigung_Deutschland_HRI-2026.pdf). This means that while SMEs play a critical role in the supply chain, they rarely control final contracts or procurement relationships. This affects their access to finance since SMEs cannot currently use government contracts directly as collateral.

Second, the financing gap will increase as NATO targets rise from 2% to 5% of GDP. Much of this expansion in spending is forecast to be consumption (i.e. equipment procurement) rather than investment requiring different (non- VC) mechanisms for delivering private capital to the market (https://www.imk-boeckler.de/fpdf/HBS-009302/p_imk_pb_207_2026.pdf).

Third, the way in which defence procurement is currently structured, and its interface with private credit, means that the growth effects of increases in German financing for defence are likely to be limited (https://www.vwl.uni-mannheim.de/media/Lehrstuehle/vwl/Krebs/Studie_militaer_final-1.pdf). A more flexible approach to SME and supply chain financing will help address this issue and private credit is a core part of the solution.

To summarise there are still major difficulties for German SMEs without targeted financial instruments, increased defence spending risks:

concentrating funding in large primes

leaving SME supply chains undercapitalised

slowing the expansion of Europe’s defence industrial capacity.

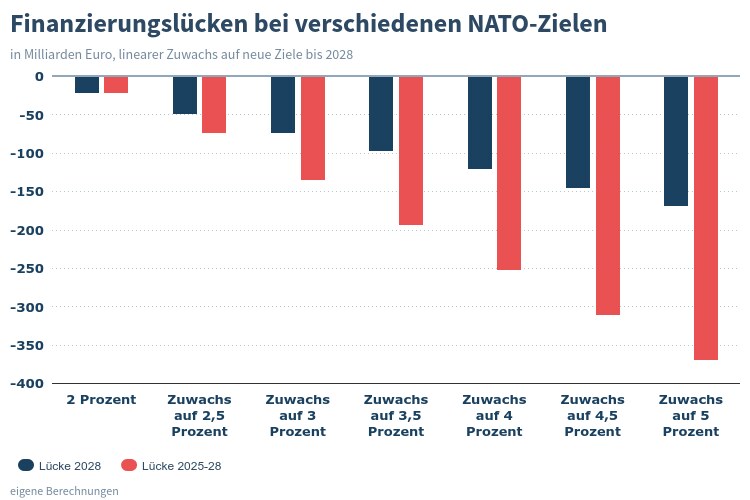

There is a hole in financing for German SMEs under different assumptions for %GDP contributions to NATO according to Hubertus Bardt (IW Köln, January 2025):

Bardt, H. (IW Köln, Jan 2025) — Finanzierungslücken bei verschiedenen NATO-Zielen: projected funding gaps in billions of euros as spending targets rise from 2% to 5% of GDP. Own calculations. Note: predates the 2026 large-scale expansion in German defence financing.

Schularik & Binder (2026) argue that Germany has dedicated money to defence spending but needs to be able to match its financial strengths with the capacity create long term scalability against the likelihood of long-term conflict. Key is the capacity for rapid expansion in productive capability which is not evident at the moment; Germany should be open to the idea of collective defence finance because:

Need to frontload spending in order to scale quickly for deterrence

Guns vs butter elsewhere in Europe because of fiscal constraints not helping Europe to scale as quickly as it could and this will affect Germany

Joint liabilities ensure European financial autonomy

Germany has a per-capita investment gap in defence SMEs compared to the US and France. The US spends around €510 per head on defence SMEs, the French €108 and Germany €90. Thus, while the Deutschlandfonds is to be welcomed, it is too little without significant private sector engagement. The Association of German Start-ups argues that there should be an acceleration of private credit and debt-based finance in order to enable rapid scale up across German industry. The German Chamber of Commerce and Industry (IHK) agrees that there needs to be an effective financing structure to meet the requirements for rapid scale-up and international growth that the defence industry needs but does not prescribe debt financing alone.

The core argument is that the spending scale-up flows primarily to large primes through procurement contracts. SMEs need a different mechanism — patient, guaranteed, intermediated debt — which is precisely what a multilateral bank structure provides and what the market alone is still not delivering as of mid-2025.

LBBW internal research (2026) highlights the following challenges

Industrial scale-up will require significant CapEx: higher volumes imply investment in production lines, machinery, tooling, testing infrastructure, certification capacity, and broader industrial ramp-up.

Bridge financing is a core constraint: interim funding needs are rising materially, especially for working capital, order pre-financing, inventory build-up, and guarantee lines.

Backlog growth increases financing pressure: order backlog at European defence companies rose from €103bn in 2017 to €291bn in 2024 (+183%). This means suppliers must finance production expansion well before cash is collected.

The bottleneck sits in the supply chain, not only at prime level: large contractors rely on a broad base of mid-sized suppliers, so funding constraints at SME level can directly slow delivery capacity.

SMEs are structurally more exposed: key constraints include limited capital reserves, limited staffing, and dependence on larger customers. That makes bridge financing and liquidity support particularly relevant for mid-sized firms.

The economic impact is heavily supply-chain driven: annual defence investment in NATO Europe translates into roughly €149bn of gross value added, with about €75bn generated indirectly along the supply chain.

Employment effects are also concentrated beyond the primes: around 1.99 million jobs are linked to this investment effect in NATO Europe, including about 971,000 indirect jobs in the supply chain.

Innovation financing is part of the picture: R&D spending by European defence companies has increased by 54% since 2018, pointing to additional financing needs in R&D, prototyping, qualification, and industrialisation of new technologies.

Annual gross value added in NATO Europe is approximately €149 billion.

Around €75 billion of this value added is generated along the supply chain.

Direct defence production accounts for about €40 billion of gross value added.

Supplier industries therefore generate almost twice as much value added as direct defence production.

Suppliers account for roughly 50% of total gross value added (€75bn out of €149bn).

When comparing only direct and indirect value added, suppliers account for about 65% (€75bn out of €115bn).

According to Deutsche Bank general credit constraints interact with procurement in ways that disproportionately restrict access to finance for defence businesses. To summarize, SMEs have to finance component sourcing, materials and inventory, certification and testing and scaling from their own revenues before they receive payment from primes or government. Since short term credit has declined by 0.9% year on year to December 2025 and medium-term lending by around 3.1% this is likely to cause real challenges for scaling the SME defence industrial base quickly. According to the Deutsche Bank multilateral mechanisms for addressing the SME cross-border supply chain funding gap were developed during the pandemic and can be used as a benchmark for a multilateral funding framework now.

Conclusion

The evidence reviewed in this document suggests that Germany’s defence financing challenge is not simply one of increasing public spending, but of ensuring that financial flows reach the SME-driven supply chains that underpin the country’s defence industrial capacity. While recent policy changes have significantly expanded fiscal space for defence, the mechanisms required to translate this spending into scalable industrial production remain incomplete. SMEs face tightening credit conditions, limited access to venture capital, and structural barriers in procurement that prevent them from leveraging government contracts to secure financing. Given that suppliers generate a substantial share of defence-related economic value added and are responsible for much of the sector’s innovation and manufacturing capacity, these financing constraints risk becoming a critical bottleneck in Europe’s ability to expand defence production. Addressing this gap will require new financing structures that combine public guarantees, private credit, and collaborative European financing mechanisms capable of providing the long-term, intermediated capital needed to support SME-led scale-up across the defence industrial base.

Artillery ammunition prices have risen several hundred percent since 2021. Dr. Rebecca Harding on how defence inflation is eroding NATO military capability.

Defence spending alone has modest and short-lived effects on growth. Dr. Rebecca Harding on why the STRUCTURE of defence finance is what turns spending into sustained resilience.

Sweden’s defence industrial model is highly capable but structurally constrained. Dr. Rebecca Harding examines why 380 firms sit alongside acute SME access-to-finance risk.

Germany’s defence SMEs face a systemic access-to-finance challenge that has become a strategic vulnerability. Dr. Rebecca Harding on the evidence and the mechanisms.