85% of Norway’s defence firms are SMEs, yet 70% of revenues sit with just four companies. Dr. Rebecca Harding on why this concentration matters — and how multilateral finance could rebalance it.

Dr. Rebecca Harding | April 2026

Executive Summary

Norway’s defence industry is an SME-dominated but highly concentrated system: Around 85% of Norway’s defence firms are SMEs, yet approximately 70% of revenues are concentrated in just four companies, creating a structural divide between innovation and scale.

Rapid growth in the defence industry is driven by exports and policy: The sector is expanding quickly, underpinned by rising defence spending (towards 5% of GDP by 2036) and strong export demand in niche, high-end capabilities such as missiles, naval systems and autonomous technologies.

There is a persistent SME financing gap: Despite strong public finances, SMEs face limited access to bank lending, export finance is skewed towards large firms, and procurement structures do not consistently improve working capital conditions.

There are clear scaling and supply chain constraints: Rigid procurement systems and weak integration between SMEs and primes inhibit scale-up, reducing supply chain resilience and slowing the transition from innovation to production.

The role for DSRB is to correct the market failures that mean that SMEs find it hard to access supply chains: A multilateral financing mechanism could unlock private capital, support SME scale-up, and strengthen industrial resilience, particularly given Norway’s limited access to EIB financing as a non-EU country.

Introduction

Norway’s defence industrial base is highly specialised, export-oriented and SME-dominated, but structurally constrained by financing gaps, supply chain rigidities and dependence on a small number of large primes. Around 85% of firms are SMEs, yet just four companies account for approximately 70% of sector revenues, creating a dual structure in which innovation is widely distributed but scale and market access are concentrated.

The sector has experienced rapid growth, driven by rising defence spending and export demand, particularly in high-end systems such as missiles, naval technologies and autonomous capabilities. Government policy reflects a strong commitment to expanding productive capacity, with long-term defence spending projected to reach 5% of GDP and targeted funding for SMEs and industrial scaling. However, this expansion is occurring within a system characterised by fragmented supply chains and limited integration between SMEs, start-ups and prime contractors.

Despite substantial public funding and a large sovereign wealth fund, access to finance remains a critical constraint for SMEs. Commercial banks remain reluctant to lend to defence businesses, export finance mechanisms are skewed towards larger firms, and procurement structures do not consistently translate into improved working capital conditions. At the same time, Norway’s status as a non-EU country limits access to European Investment Bank financing, increasing the cost of capital for domestic firms.

These dynamics create a structural scaling challenge: while Norway’s SMEs are globally competitive in niche technologies, they face barriers in transitioning from innovation to industrial production. As such, these market failures risk limiting supply chain resilience and constraining the country’s ability to rapidly expand defence.

A multilateral financing mechanism such as a Defence, Security and Resilience Bank (DSRB) would directly address these constraints by providing guarantees, long-term capital and dedicated financial instruments targeted at SMEs. This would complement Norway’s existing strengths—innovation, export capability and strong public finances—by unlocking private sector financing, improving supply chain resilience and accelerating industrial scale-up in support of both national and allied security objectives.

Norway’s defence sector

Norway’s defence industry is niche and specialised with a strong innovative and technological base in systems capability and naval defence. The domestic industry focuses on Command-and-Control systems, System Integration, Autonomous Systems, Missile Technology, Underwater Sensors, Ammunition and remote-controlled weapons delivery mechanisms.[1]

Norway’s defence industry is highly collaborative internationally, not least because of its highly specialised areas of focus.[2]

Norway’s defence industry is the largest defence industrial base outside the EU in Europe. Its largest defence business, Kongsberg Gruppen, had a turnover of around NOK 48.9bn in 2024. Kongsberg Gruppen, Kongsberg Defence, Nammo and Vard between them produce air defence systems, artillery ammunition and naval solutions that are critical both to EU and NATO security in the High North in particular[3] but also in Ukraine. The Norwegian government has committed NOK 3.2bn in funding for the purchase of F-16 fighter jets, laser-guided missiles and ground-based air defences.[4]

Norwegian Armed Force are tasked with contributing to economic security as well as defence and security in that they are tasked with ensuring that the industry is competitive and contributes to economic growth.[5]

The FSi, the Norwegian defence industry association, has some 300 member companies, some 85% of which are SMEs.

Norway’s defence industry is highly concentrated. The Norwegian Defence Research Establishment annual report identified 34% revenue growth and 85% increase in R&D allocation in 2024. Although the industry is dominated by SMEs, just four companies accounted for 70% of defence sector revenues.

Large Primes such as Kongsberg have highly standardised approaches to their supply chains which make accessing them very difficult. This is however a potential vulnerability in creating resilience because, with structured programmes like this, there is limited scope for SMEs to be substituted during a production or delivery process.[6]

However, Norway’s policy and defence industry players recognise the need for close collaboration between the innovation base in defence and large primes in an era where modern warfare is defined increasingly by autonomous capability and where the defence industry itself is regarded as fragmented.[7] The Innovation and Industrial Development arm of FFi is focused on improving links between the parts of the ecosystem in order to strengthen these relationships deemed as critical to national security.[8] Norway’s market, along with others in the Nordic countries, stands to benefit from the mechanisms that are inherent to the European Defence Fund.[9]

The rapid rate of growth in material and equipment and software is encouraging private equity into Tier 2 and 3 supply chains according to PwC.[10]

Norway’s defence spending and policy

Norwegian defence spending is increasing very rapidly. The Langtidsplan for forsvarssektoren was reinforced in March 2026 by an additional NOK 115bn through 2036, including NOK 31bn committed by 2030, with defence spending projected to reach 3.5% of GDP by 2035.[11] At the same time, defence exports have risen strongly: FSi reports exports of approximately NOK 19bn in 2024,[12] while Ministry of Defence reporting from April 2026 indicates exports rose to nearly NOK 21bn in 2025.[13] This creates a classic scale-up challenge: procurement ambition and export opportunity are growing faster than the balance sheets of many smaller suppliers.

Known fragmentation and a concern around supply chain resilience in Norway underpins the new defence funding plan whose objective is to increase productive capability in the industry itself. The government is prioritising a long-term and integrated approach with a particular focus on NASAMS air defence systems and military high explosives, innovative technologies creating operational advantage and artillery ammunition.[14]

The Norwegian government’s long term defence plan committed NOK 1,624bn including an additional increase of NOK 600bn to sovereign defence over the next 12 years.[15] An additional NOK 115bn (or $12bn) means that the country’s commitments to its defence should reach the aspired 5% of its GDP by 2036[16] as it is already at 3.4% of its GDP in 2026.[17]

There is a strong commitment to building productive capacity in Norway and the expansion in expenditure includes the infrastructure to build responsiveness and agility.[19] Norway’s policy is to regard collaboration with international partners as essential to its security and resilience.[20]

Perhaps because of the dominance of larger businesses and the dependency on imports for larger capability, many small firms do struggle still with access to finance, not least because of Norway’s commitment to strong sustainability principles.[21] Many of the private banks remain reluctant to invest in the defence sector and a review of the Sovereign Wealth Fund is being undertaken in order that it can overtly invest in defence entities after a 21 year ban.[22]

The new procurement regulations do simplify regulations and make larger sums available in advanced payments.[23]

Norway’s exports and innovation structures

Around 90% of Norway’s defence industry sales in 2022 were to customers outside of Norway.[24]

In 2024, Norway exported $638m in arms and ammunition making it the 12th largest exporter in the world.[25] This is a lower number than the government suggests because it is based on the SIPRI methodology.[26]

Exports are driven by Kongsberg which exports the F-35 fuselage and surface-to-air missile systems and by Nammo which is a major ammunitions business supplying everything from rifles to 155mm shells.[27]

Norwegian defence exports increased by nearly 40% in 2025 alone.[28]

To deliver on sustained export growth, Eksfin, the Norwegian Export Credit Agency, has been funding export finance contracts, such as Kongsberg defence system exports to Poland.[29]

Innovation Norway provides funding for research-based defence projects.[31]

Finance

The country does not face a general shortage of SME credit. OECD data show outstanding SME loans in Norway reached NOK 856bn in 2023, representing approximately 39% of total business lending, with more than 82% of SME loans classified as long-term.[32] Norges Bank characterises Norwegian banks as well-capitalised, resilient and fully capable of supplying credit.[33] The issue is therefore not whether finance exists in Norway, but whether it reaches defence SMEs in a form that matches the sector’s needs.

Norway’s niche businesses are highly attractive to investors outside of Norway.[34]

Norway’s $2.2tn sovereign wealth fund is the largest in the world.[35]

Because Norway has a strong international collaborative culture and provides niche specialisms based on topographical considerations it has close partnerships between international providers, its own defence sector, government and innovation. Since 2021 Norway has coordinated six programmes worth around €114m.[36]

Norwegian businesses are not commonly eligible for EIB guarantees as Norway is a third country.[37] This affects the High North[38] and creates cost disadvantages.[39]

SMEs are eligible for co-funding to develop innovative dual-use technologies if they have already accessed private finance.

Export finance and guarantees are central to the Norwegian model. Eksfin was established in its current integrated form following the merger of Eksportkreditt Norge and GIEK in January 2021.[40] A cooperation agreement with DNB increased working capital guarantee credit-line limits from NOK 1bn to NOK 1.5bn, alongside a NOK 5bn guarantee for banks announced in 2024.[41]

The Roadmap for Expanding Production Capacity in the Defence Industry (2025)[42] treats long-term government contracts as the state’s most powerful instrument for inducing industrial investment. Norway participates in the EU’s Act in Support of Ammunition Production (ASAP)[43] and NOK 342m was earmarked specifically for smaller Norwegian companies.[44] Innovation Norway operates a common access gateway for civilian businesses seeking to enter the defence supply chain.[45]

Conclusions for DSRB

The DSRB addresses a specific market failure: the absence of long-tenor, risk-tolerant capital for defence SME scale-up.[46]

There is surprisingly little explicit material around defence SME working capital support or innovation in government policy that is publicly available.

Even the Primes have acknowledged that rigid procurement protocols and structures for onboarding make it challenging for new SMEs to work within their supply chains.

A multilateral defence funding model directly addresses this challenge.

Norway’s SWF provides a core “lender of last resort” function to the Norwegian government.

The DSRB would support Norwegian government objectives to scale innovative and productive capability by providing guarantees to banks and dedicated financial instruments for defence.

Norway’s defence businesses face constraints on accessing any available EIB money as Norway is a third country. This is where DSRB has a major advantage.

Appendix

A note on terminology. The Defence, Security and Resilience Bank (DSRB) referred to throughout this briefing is a proposed multilateral or jointly governed specialist lending facility designed to provide long-tenor, cross-border and guarantee-backed capital to defence SMEs across participating NATO and allied nations.

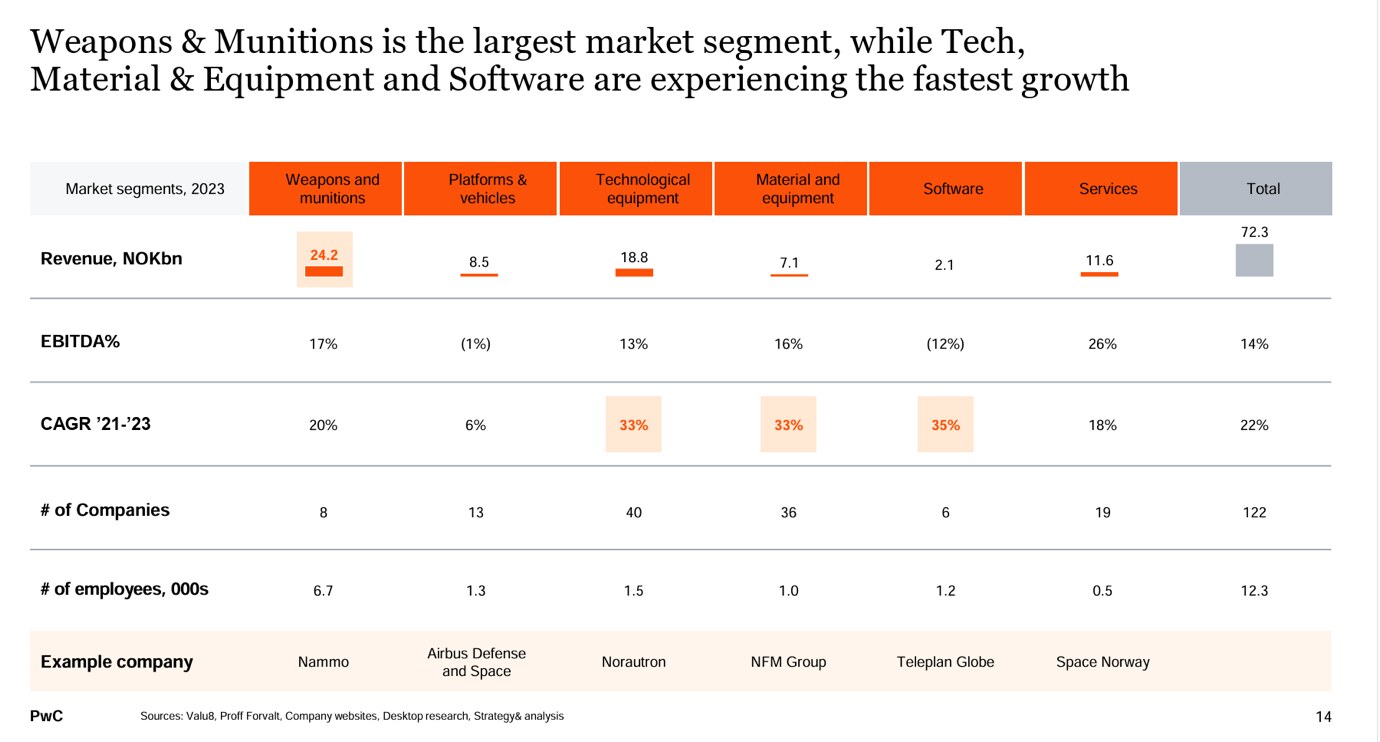

PwC (2025) — Weapons & munitions is the largest market segment, while Tech, Material & Equipment and Software are experiencing the fastest growth. Norwegian defence sector segmentation 2023. Sources: Valu8, Proff Forvalt, Company websites, Desktop research, Strategy& analysis.

A note on sources and definitions. All quantitative claims are drawn from primary institutional sources. All SME figures apply the EU standard definition (fewer than 250 employees; annual turnover not exceeding €50m or balance sheet not exceeding €43m),[47] which is consistent with Norwegian statistical practice and OECD reporting conventions.[48] Defence export figures follow the Norwegian Ministry of Foreign Affairs reporting methodology.[49]

Artillery ammunition prices have risen several hundred percent since 2021. Dr. Rebecca Harding on how defence inflation is eroding NATO military capability.

Defence spending alone has modest and short-lived effects on growth. Dr. Rebecca Harding on why the STRUCTURE of defence finance is what turns spending into sustained resilience.

Sweden’s defence industrial model is highly capable but structurally constrained. Dr. Rebecca Harding examines why 380 firms sit alongside acute SME access-to-finance risk.

Germany’s defence SMEs face a systemic access-to-finance challenge that has become a strategic vulnerability. Dr. Rebecca Harding on the evidence and the mechanisms.